What is the 50 30 20 rule of budgeting?

Those will become part of your budget. The 50-30-20 rule recommends putting 50% of your money toward needs, 30% toward wants, and 20% toward savings. The savings category also includes money you will need to realize your future goals.

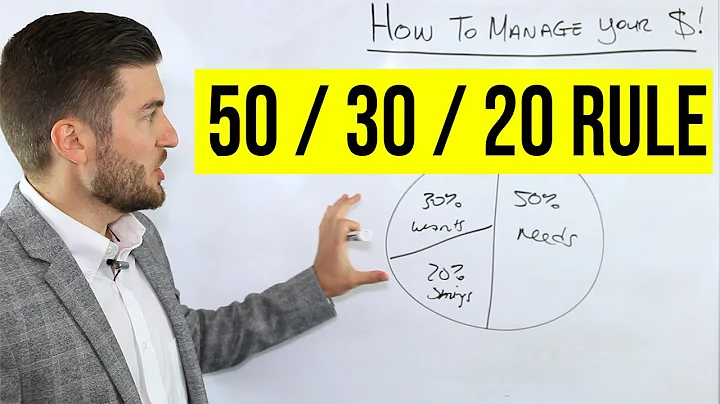

A 50 30 20 budget divides your monthly income after tax into three clear areas. 50% of your income is used for needs. 30% is spent on any wants. 20% goes towards your savings.

Our 50/30/20 calculator divides your take-home income into suggested spending in three categories: 50% of net pay for needs, 30% for wants and 20% for savings and debt repayment.

For this reason, you can anticipate having a tough time bringing about substantial transformations in your organization. As a rule of thumb, 20% of your people will support your efforts to initiate change, 50% will be undecided, and the remaining 30% will resist you.

At least 20% of your income should go towards savings. Meanwhile, another 50% (maximum) should go toward necessities, while 30% goes toward discretionary items.

You allocate 50% of your post-tax income to “needs” and another 30% to “wants.” That leaves you with at least 20% of your net income that you're able to save or use to pay down existing debt.

The Takeaway

Using them, you allocate your monthly after-tax income to the three categories: 50% to “needs,” 30% to “wants,” and 20% to saving for your financial goals. Your percentages may need to be adjusted based on your personal circ*mstances and goals.

Some Experts Say the 50/30/20 Is Not a Good Rule at All. “This budget is restrictive and does not take into consideration your values, lifestyle and money goals. For example, 50% for needs is not enough for those in high-cost-of-living areas.

Here, 50 per cent of your income should go towards living expenses (needs), like household expenses, groceries; 20 per cent (savings) towards savings for your short, medium, long-term goals; and 30 per cent towards spending (wants), including outings, food and travel.

The 50/30/20 rule originates from the 2005 book, “All Your Worth: The Ultimate Lifetime Money Plan,” written by current US Senator Elizabeth Warren and her daughter, Amelia Warren Tyagi.

Does the 50/30/20 rule work?

The 50/30/20 rule can be a good budgeting method for some, but it may not work for your unique monthly expenses. Depending on your income and where you live, earmarking 50% of your income for your needs may not be enough.

However, the key difference is it moves 10% from the "savings" bucket to the "needs" bucket. "People may be unable to use the 50/30/20 budget right now because their needs are more than 50% of their income," Kendall Meade, a certified financial planner at SoFi, said in an email.

50% of your net income should go towards living expenses and essentials (Needs), 20% of your net income should go towards debt reduction and savings (Debt Reduction and Savings), and 30% of your net income should go towards discretionary spending (Wants).

Applying the 50/30/20 rule would give them a monthly budget of: 50% for mandatory expenses = $2,500. 20% to savings and debt repayment = $1,000. 30% for wants and discretionary spending = $1,500.

Are you approaching 30? How much money do you have saved? According to CNN Money, someone between the ages of 25 and 30, who makes around $40,000 a year, should have at least $4,000 saved.

The rule was popularized by U.S. Sen. Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2006 book, “All Your Worth: The Ultimate Lifetime Money Plan.”

What is a 'pay yourself first' budget? The "pay yourself first" method has you put a portion of your paycheck into your savings, retirement, emergency or other goal-based savings accounts before you do anything else with it. After a month or two, you likely won't even notice this sum is "gone" from your budget.

Step 6: Decide how and how much you want to save each budget cycle. There are a lot of ways to decide how much you would like to put aside. One common method is the 50/30/20 rule. You use 50 percent of your earnings on needs, 30 percent on nonessentials, and save 20 percent.

If you're looking for a ballpark figure, Taylor Kovar, certified financial planner and CEO of Kovar Wealth Management says, “By age 30, a good rule of thumb is to aim to have saved the equivalent of your annual salary. Let's say you're earning $50,000 a year. By 30, it would be beneficial to have $50,000 saved.

- 50% for mandatory expenses = $2,000 (0.50 X 4,000 = $2,000)

- 30% for wants and discretionary spending = $1,200 (0.30 X 4,000 = $1,200)

- 20% for savings and debt repayment = $800 (0.20 X 4,000 = $800)

What are the 3 P's of budgeting?

Introducing the three P's of budgeting

Think of it more as a way to create a plan to spend your money on things that matter to you. Get started in three easy steps — paycheck, prioritize and plan.

Taxable income includes wages, salaries, bonuses, and tips, as well as investment income and various types of unearned income.

Saving $1,000 per month can be a good sign, as it means you're setting aside money for emergencies and long-term goals. However, if you're ignoring high-interest debt to meet your savings goals, you might want to switch gears and focus on paying off debt first.

Saving $1,500 per month may be a good amount if it's feasible. In general, save as much as you can to reach your goals, whether that's $50 or $1,500. You could speak with a certified financial planner to help develop a plan for your finances if you aren't sure how much money to save regularly.

Alternatives to the 50/30/20 budget method

For example, like the 50/30/20 rule, the 70/20/10 rule also divides your after-tax income into three categories but differently: 70% for monthly spending (including necessities), 20% for savings and for 10% donations and debt repayment above the minimums.